Search Virginia Property Tax Records

Virginia property tax records are public information maintained by the Commissioner of the Revenue and the Treasurer's office in each county and independent city across the state. These records cover real estate assessments, tax bills, payment history, and land book data going back many years. Whether you need to look up a current assessment, find out what a property sold for, or check the tax status on a parcel, this site gives you a starting point for searching property tax records in any part of Virginia.

Virginia Property Tax Records Overview

Virginia Property Tax Records

In Virginia, property tax records are local records. Each of the state's 98 counties and 39 independent cities runs its own assessment and tax collection system. The Commissioner of the Revenue handles assessments. The Treasurer collects the bills. Circuit court clerks maintain land books. You deal with the local office for the jurisdiction where the property sits, not a central state agency.

The Virginia Department of Taxation sets policy and oversees compliance, but it does not collect real estate taxes directly. Local governments do that. The department's website at virginia.gov offers general guidance on tax law and programs, but your first stop for any specific parcel should be the Commissioner of the Revenue in that county or city.

The Virginia Department of Taxation administers the tax laws of the Commonwealth with the goal of supporting government services for all Virginia citizens. Property tax records tied to each parcel include the assessed value of land and improvements, the tax rate applied, the bill amount, and the payment status. These records are open to the public under Virginia law.

The screenshot below shows the Virginia Department of Taxation homepage, which serves as the state's central tax administration portal.

The agency provides resources for property owners who need general guidance on Virginia's tax structure and how local tax programs connect with state law.

How Real Estate Assessment Works in Virginia

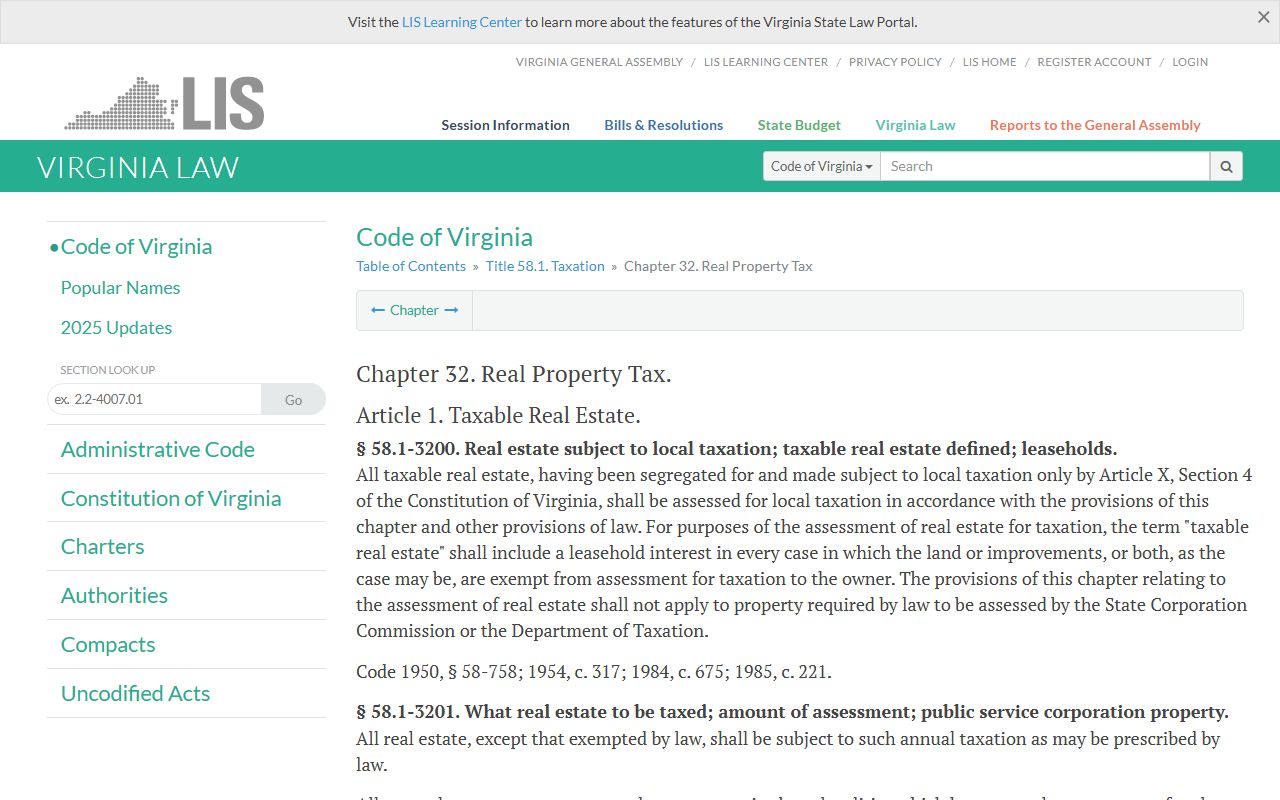

Under Virginia Code Chapter 32 of Title 58.1, all taxable real estate must be assessed at 100 percent fair market value. There are no assessment ratio tricks like you see in some other states. Every general reassessment or annual reassessment has to reflect what a willing buyer would pay a willing seller on the open market. The State Corporation Commission and the Department of Taxation certify public service corporation property values to counties and cities, but most residential and commercial parcels are valued by local assessors using mass appraisal systems and sales analysis.

Some localities reassess every year. Others do it every four or six years. The cycle depends on what the local government has adopted. Counties and cities that reassess annually tend to have more current data and smoother year-to-year changes. Those that reassess less often may see larger jumps when the cycle comes around. Either way, § 58.1-3200 requires fair market value to be the standard.

The screenshot below shows the full text of Virginia's Real Property Tax statutes in Chapter 32, which governs how local governments assess and tax real estate across the state.

Reviewing the full chapter is useful for anyone who wants to understand the legal framework behind how their property tax bill gets calculated and how to push back if they believe it's wrong.

Multi-unit residential property rented primarily to residential tenants is assessed without regard to potential conversion value. This matters in markets where apartment buildings might attract condominium converters. Virginia law protects renters and owners from inflated assessments based on hypothetical use rather than actual market conditions. Leasehold interests in exempt real property are assessed to the lessee using a sliding scale based on remaining lease term, reducing the assessed value by two percent for each year the remaining term is less than 50 years, up to an 85 percent maximum reduction.

The full text of Title 58.1 covers all Virginia tax law, with Subtitle III specifically addressing local taxes including real property tax, personal property, and enforcement and collection.

Access to Property Tax Records in Virginia

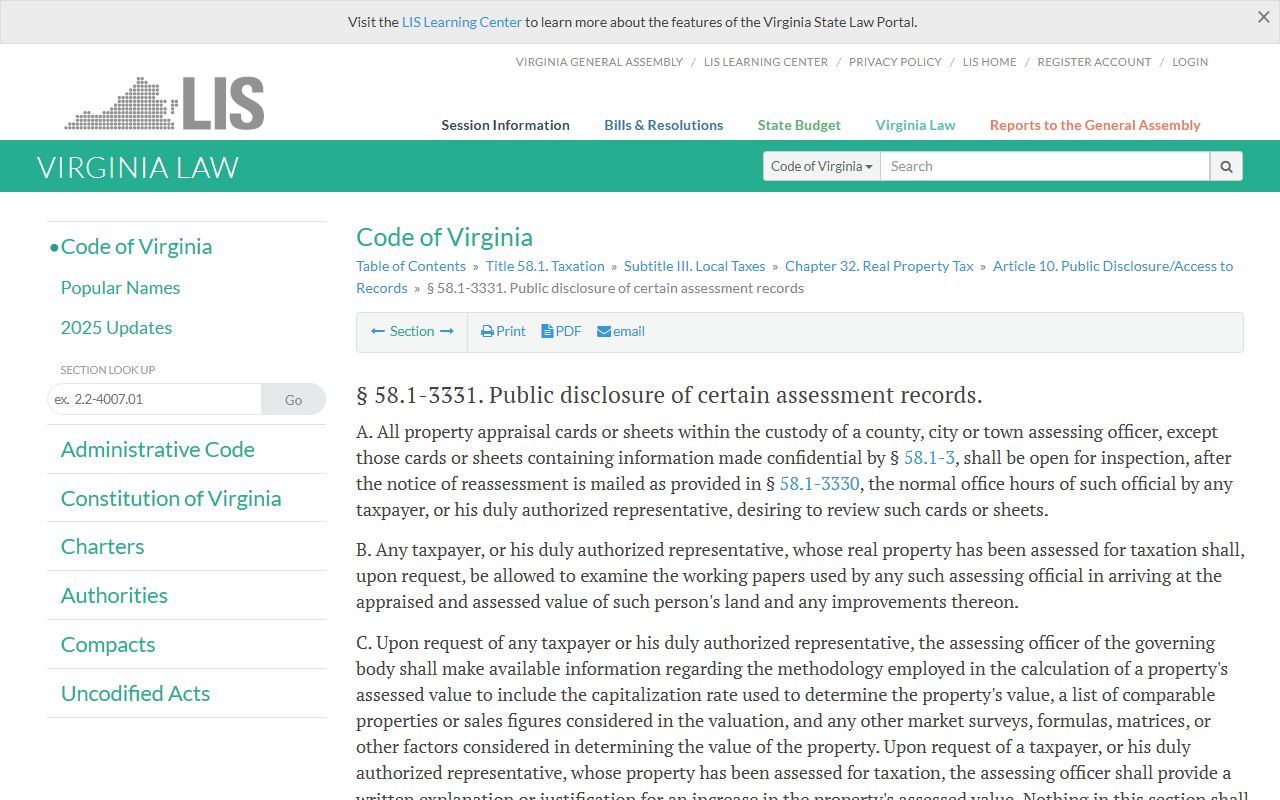

Virginia law gives the public clear rights to view property assessment records. Under § 58.1-3331, all property appraisal cards or sheets kept by local assessing officers must be open to public inspection during regular business hours. You do not have to own the property to look at the records. Anyone can walk in and ask to see how a parcel was valued.

The law goes further for property owners. If you own real property, you have the right to inspect and copy the assessment records for your parcel. That includes the appraised value of land and improvements, the calculations used to reach that value, and the methodology applied. You also have the right to see comparable property data used in determining your assessment. This gives you the tools to check whether your property is being treated the same as similar properties in the same area.

The screenshot below shows the text of Virginia Code § 58.1-3331 on public inspection of property assessment records.

Assessing officers must provide reasonable access and may charge a copying fee, but that fee cannot exceed the actual cost of reproduction. This keeps access affordable for any property owner who needs documentation for an appeal or for their own records.

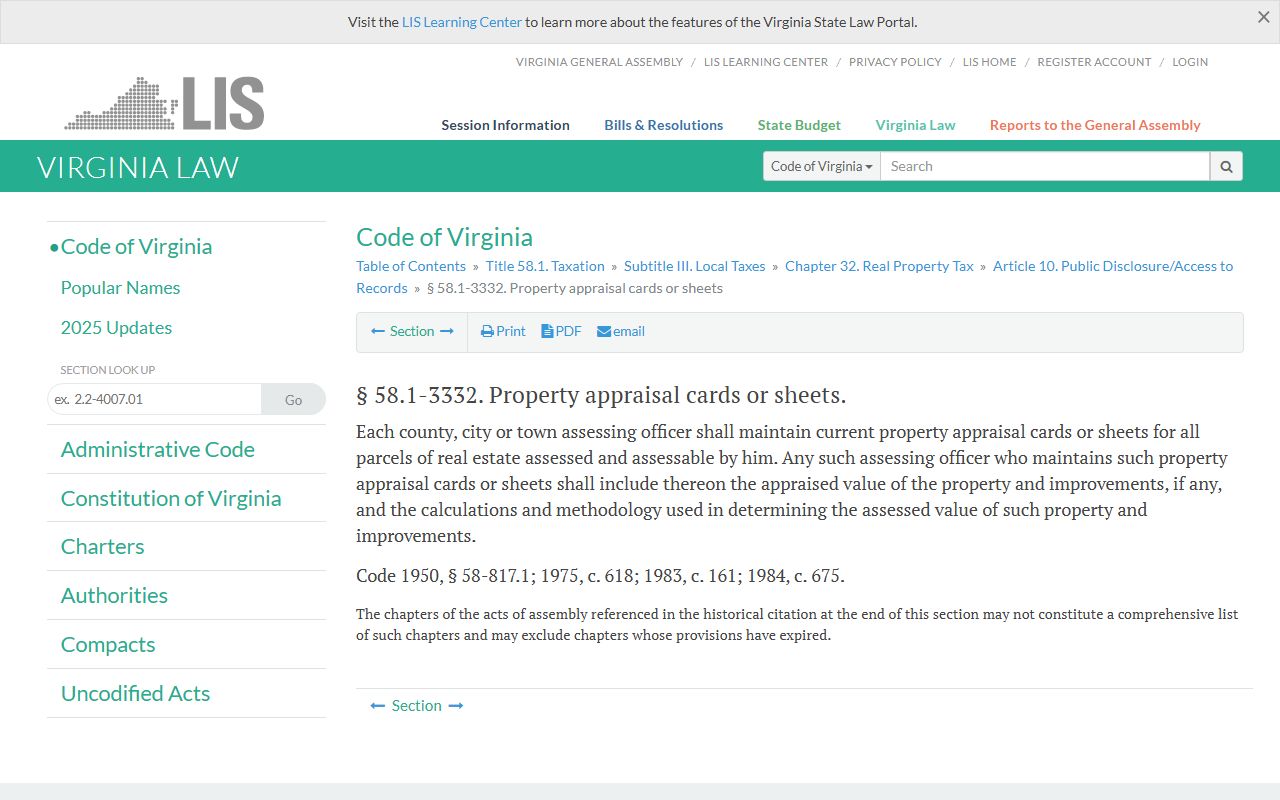

Beyond public inspection rights, § 58.1-3332 requires each assessing officer to maintain current property appraisal cards or sheets for every parcel in the jurisdiction. These cards must include the appraised value of the property and improvements as well as the calculations and methodology used. The screenshot below shows this statute in detail.

These appraisal records are subject to the same public inspection rights established in § 58.1-3331, allowing taxpayers to understand how their property was valued.

Note: If you need records going back many years, some older land books may only be available through the circuit court clerk's office rather than the Commissioner of the Revenue.

Assessment Change Notices

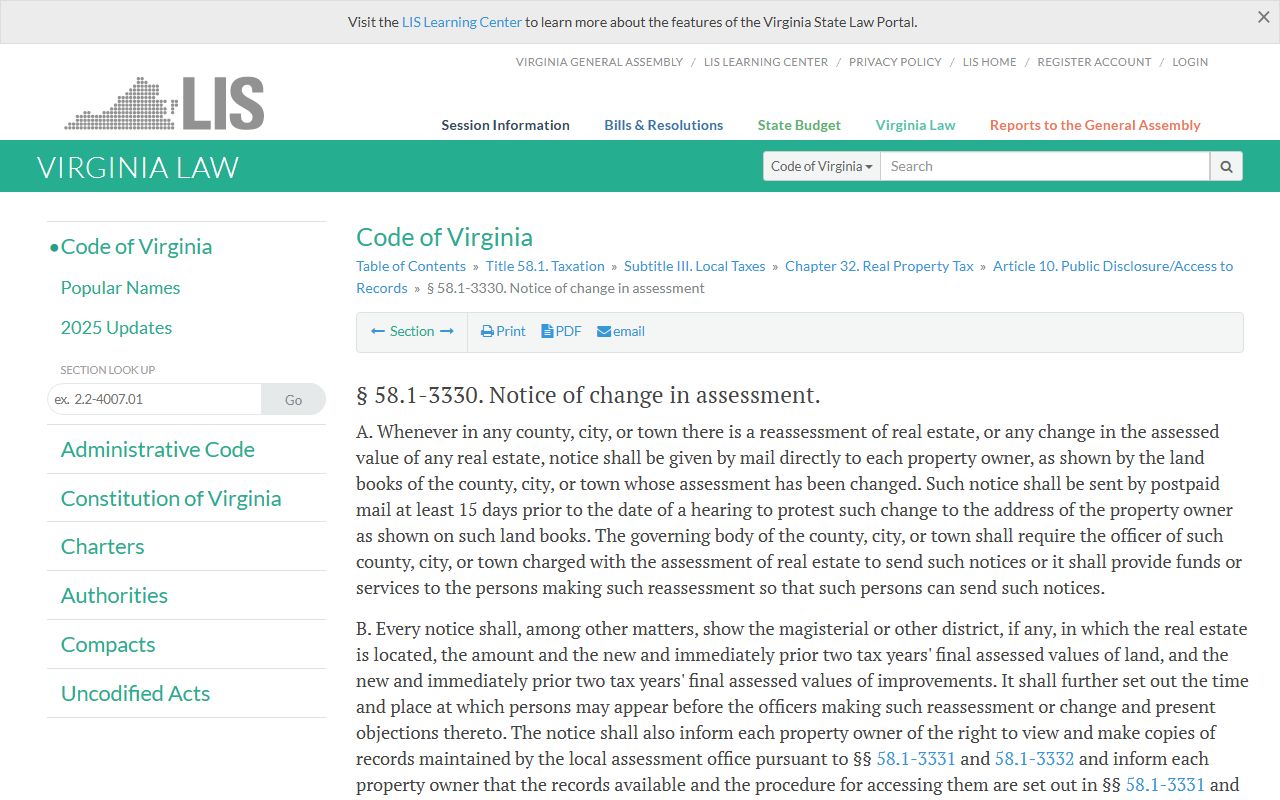

When your property assessment changes, Virginia law requires the local government to tell you. Under § 58.1-3330, the assessing officer must mail a notice to each property owner at least 15 days before any hearing to protest the change. The notice goes to the address shown in the land books. If you've moved and haven't updated your address with the local office, you might miss it.

The notice has to include specific information. It must show the magisterial or other district, the new assessed values for land and improvements, and the final assessed values from the prior two tax years. It also must tell you the time and place for presenting objections. If the tax rate has already been set, the notice must include the current rate, the prior two years' rates, the new tax levy based on current rates, prior year levies, and the percentage changes between years. In places that do annual or biennial reassessments, if the new total assessed value would cause real property tax to rise by one percent or more, the notice must also show what rate would raise the same amount as the prior year. That's the equalized rate.

The screenshot below shows the text of § 58.1-3330, which governs how and when Virginia localities must notify property owners of assessment changes.

One detail worth knowing: if someone other than the owner receives the notice, that person must pass it along right away. Failing to do so triggers a $25 liquidated damages liability. This protects property owners who may have tenants or property managers handling their mail.

Virginia Property Tax Assessment Appeals

If you think your assessment is wrong, you have the right to appeal through the Board of Equalization. Every Virginia locality has one of these boards, and it sits independently from the assessor's office. The board can raise or lower assessments. Its job is to make sure the tax burden rests equally on all property owners in the jurisdiction.

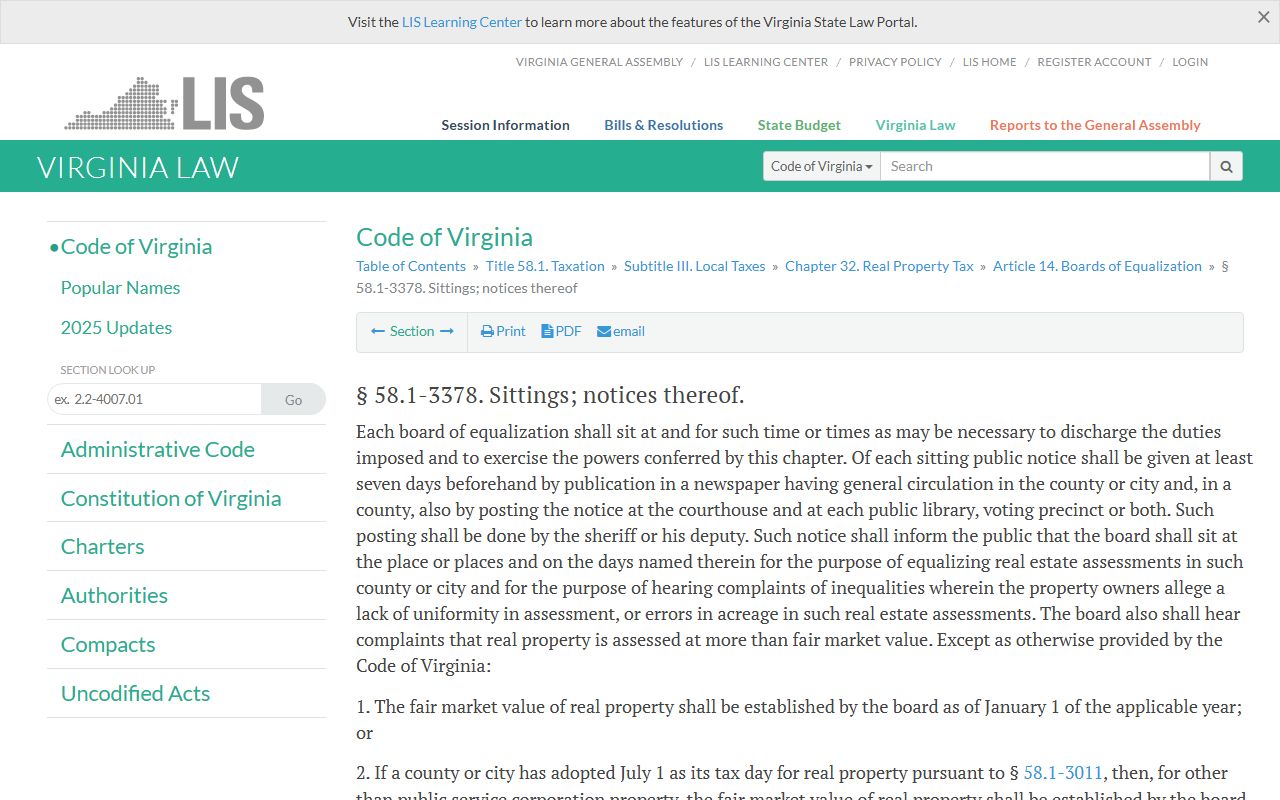

Under § 58.1-3378, each board of equalization must give public notice at least seven days before it meets. That notice goes in a local newspaper and, in counties, gets posted at the courthouse and public libraries or voting precincts. The notice must state that the board will hear complaints about inequalities, errors in acreage, and claims that property is assessed above fair market value. Fair market value is set as of January 1 of the tax year, or July 1 if the locality has adopted that date.

The screenshot below shows the text of § 58.1-3378 on Board of Equalization sittings and required public notices.

Applications can be submitted electronically or by paper. If mailed, the postmark date counts as the receipt date. For residential property appeals, you cannot be turned away just because your application lacks information, as long as you include the address, parcel number, and your proposed assessed value.

At the hearing itself, § 58.1-3379 controls the process. There is a legal presumption that the assessor's value is correct. You carry the burden of proof. You have to show by a preponderance of the evidence either that your property is valued above fair market value or that the assessment is not uniform and was not reached using generally accepted appraisal practices. For residential properties with fewer than four units, the assessing officer must provide copies of the relevant assessment records within 15 days of your written request. If they don't provide them in time, they have to present the records and explain their methodology at the hearing before you even begin your presentation.

The screenshot below shows the text of § 58.1-3379 on Board of Equalization hearings and the rules governing the appeal process.

Board members can also visit and inspect any property that's up for appeal. That's a meaningful protection, since it means the board isn't just relying on paper records.

Note: Deadlines for filing equalization appeals vary by locality. Check your assessment notice for the specific deadline that applies to your parcel.

Tax Relief and Exemption Programs

Virginia law gives local governments the authority to offer real estate tax relief to certain property owners. The two main categories are elderly and disabled residents under Article 2 of Chapter 32 and disabled veterans under Article 2.3.

For elderly and disabled residents, § 58.1-3210 et seq. allows local governing bodies to create exemption, deferral, or combination programs based on income and net worth. To qualify, you generally have to be 65 or older or permanently and totally disabled. Each locality sets its own income and asset limits, so the thresholds vary across Virginia. Some counties are generous; others set tight limits. The Commissioner of the Revenue in each county or city administers these programs and can tell you what the local rules are.

For disabled veterans, § 58.1-3219.5 through § 58.1-3219.8 provides an exemption from real estate tax on the principal residence and up to one acre of land. To qualify, the veteran must be rated at 100 percent service-connected permanent and total disability by the U.S. Department of Veterans Affairs. The surviving spouse of a disabled veteran may also qualify for continued exemption in certain situations. This is a state-mandated program, so it applies in all Virginia localities.

Surviving spouses of armed forces members killed in the line of duty are covered under § 58.1-3219.9 through § 58.1-3219.12. If the dwelling is assessed at or below the average single-family residential value in that locality, the surviving spouse can receive a full exemption. This is another statewide program that every county and city must follow.

The Virginia Department of Housing and Community Development at dhcd.virginia.gov manages programs that intersect with property taxation, including housing-related tax credit programs and incentives for historic rehabilitation. The screenshot below shows their website, which covers community development programs that affect property values and assessments across the state.

DHCD's GO Virginia program has supported 147 projects since 2022, awarding $72 million in state funding leveraged against $61 million in matching local investments across 131 localities. These development grants affect land values and the assessment base in participating communities.

Land Books and Public Records

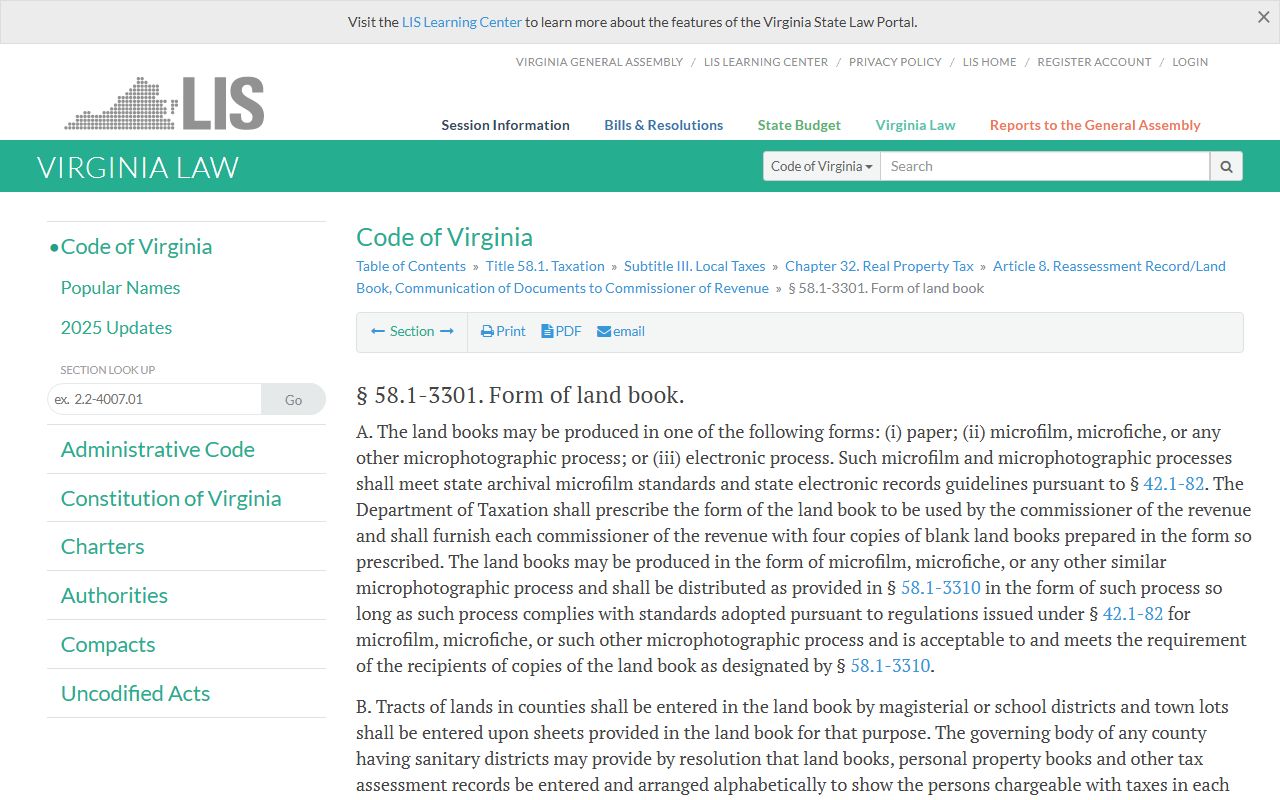

The official record of property taxation in each Virginia county is the land book. Under § 58.1-3301, the clerk of each circuit court must maintain land books containing assessments for all real estate in the county. These books are public records open to anyone who wants to look. They contain the property owner's name, a description of the property, the number of acres, the assessed value of land and improvements, and the tax amount levied.

Land books organized alphabetically may omit references to magisterial districts, which streamlines the records but can make it harder to locate parcels by district. If you are searching for records and the land book does not break things down by district, you may need to search by owner name rather than by location. This is worth knowing before you head to the circuit court clerk's office.

The screenshot below shows the text of § 58.1-3301, which establishes the land book requirement for Virginia circuit court clerks.

Land books serve as the foundation for property tax administration, appeals, and equalization proceedings. They are the starting point for researching any parcel's tax history in Virginia.

State Recordation and Transfer Taxes

When real estate changes hands in Virginia, state recordation taxes apply. Under Chapter 8 of Title 58.1, taxes are levied on deeds, deeds of trust, mortgages, and other instruments recorded in the circuit court clerk's office. The tax must be paid before the instrument is recorded. The clerk is responsible for collecting it.

The rates for deeds of trust and mortgages are tiered based on the amount of debt secured: 25 cents per $100 on the first $10 million, dropping to 16 cents on the next $10 million, then 14 cents, 12 cents, and finally 10 cents on amounts above $40 million. Some transactions also carry regional transportation fees or congestion relief fees collected at the time of recordation to fund transportation improvements in applicable districts.

Not every transfer is taxed. Virginia Code § 58.1-811 lists exemptions, including deeds to or from government agencies, deeds between spouses, and deeds of trust securing refinanced debt under certain conditions. Misrepresenting the value of property conveyed is subject to penalties. Recordation tax records are connected to property tax records because they document the sale price and the financing used in a transaction, which becomes data in the assessment process.

The screenshot below shows the text of Chapter 8 of Title 58.1 covering state recordation taxes on deeds and mortgages.

Understanding recordation taxes helps you connect the dots between what a property sold for, what was financed, and how the subsequent assessment may reflect that transaction.

Browse Virginia Property Tax Records by Location

Virginia property tax records are local records. Select a county or city below to find the specific office that handles assessments and tax collection for that area.

Virginia Counties

Each of Virginia's 98 counties has its own Commissioner of the Revenue and Treasurer handling property assessment and tax collection. Select a county to find contact information, assessment resources, and local tax records.

Virginia Cities

Virginia's 39 independent cities each have their own assessment and tax collection offices separate from surrounding counties. Select a city to find local property tax record resources.